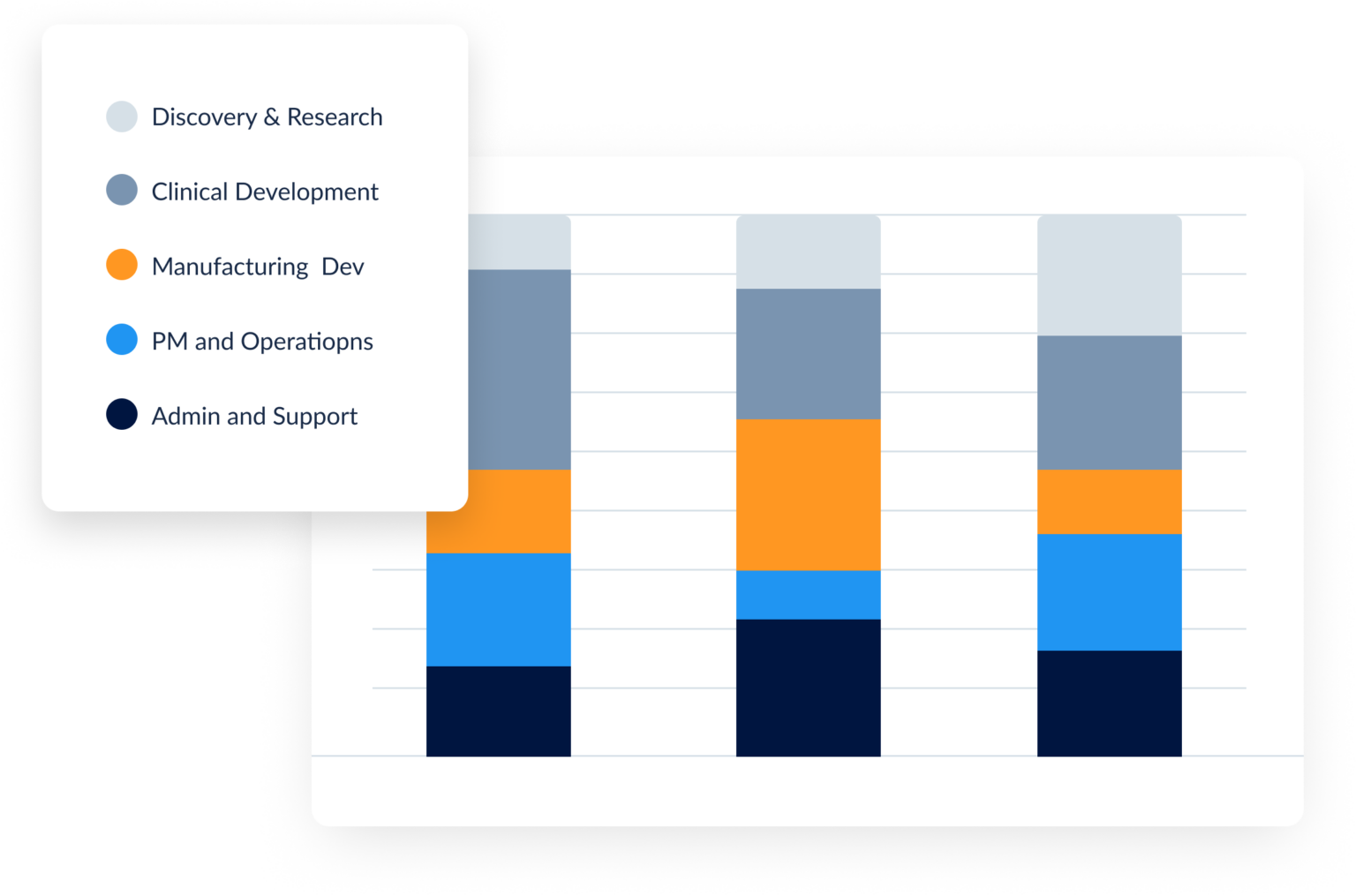

Stop losing R&D tax credits to poor documentation

- Capture eligible wages at the project level—researchers log hours against specific R&D activities, so every qualified research expense is documented for §41 credit claims

- Defend every credit claim with audit-ready records—approval workflows, timestamps, and audit trails replace the spreadsheets and retroactive estimates that trigger IRS scrutiny

- Separate qualified research from non-eligible work—finance defines the cost categories upfront, so R&D labor tracking happens at the point of entry, not months later during tax preparation